How Mortgage Rates Are Impacting the North Delta Real Estate Market in 2026

Discover how mortgage rates in 2026 are shaping North Delta real estate, buyer affordability, home prices, and smart strategies for buyers and sellers

Mortgage rates play a major role in shaping the real estate market. In 2026, buyers and sellers in North Delta are feeling the impact more than ever. Interest rates affect how much buyers can borrow, how confident sellers feel about listing their homes, and how active the overall market becomes. While rates are lower than their peak levels from recent years, they are still higher than what Canadians saw during the pandemic. This shift has changed how people approach buying, selling, and investing in real estate across North Delta.

Understanding today’s mortgage environment helps homeowners make better decisions. Whether you are planning to buy your first home, move up to a larger property, or sell your current one, knowing how mortgage rates influence the market can give you a strong advantage.

Mortgage Rate Trends in Canada and British Columbia

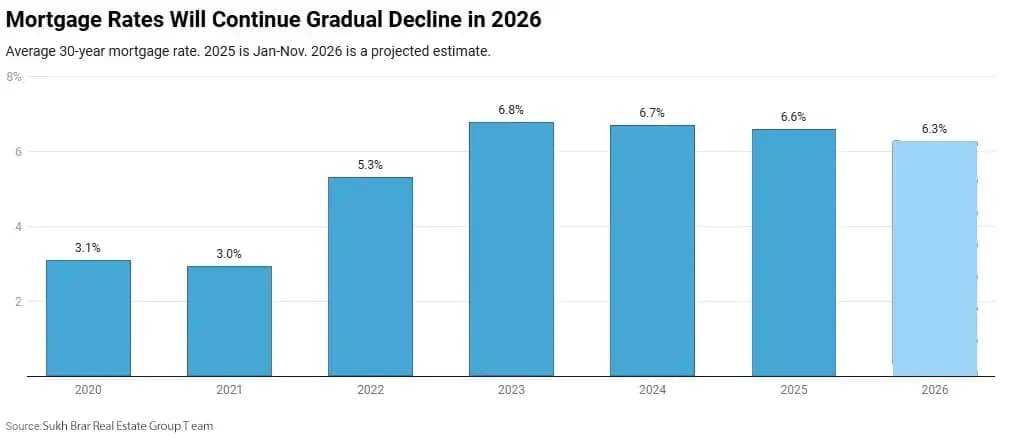

In 2026, mortgage rates in Canada are more stable compared to the sharp increases seen earlier in the decade. The Bank of Canada has slowed its rate adjustments, which has brought some confidence back to the housing market. Fixed mortgage rates remain higher than pre-pandemic levels, while variable rates offer slightly more flexibility for some buyers.

In British Columbia, and especially in communities like North Delta, this means borrowing costs are still a key factor in affordability. Buyers are more cautious with budgets and are taking extra time to plan their purchases. Many lenders are also encouraging buyers to qualify at higher stress test rates, which further affects what people can afford.

While rates are not expected to drop dramatically in the near future, the current environment offers more predictability than in previous years. This has helped some buyers regain confidence and return to the market.

Mortgage Renewals and Changing Monthly Payments

One of the biggest challenges in 2026 is mortgage renewal. Many homeowners in North Delta locked in very low interest rates several years ago. Now, as those mortgages expire, they are renewing at much higher rates. This leads to higher monthly payments, even if their mortgage balance has decreased.

For many households, this adjustment means tightening budgets or reconsidering future plans. Some homeowners delay moving because they do not want to give up their lower mortgage balance or take on a higher interest rate with a new property. Others explore refinancing options or extend amortization periods to keep payments manageable.

This renewal pressure is shaping the market by reducing the number of homes for sale, which impacts supply and competition.

How Mortgage Rates Affect Buyer Affordability

Higher mortgage rates reduce how much buyers can borrow. Even a small increase in interest rates can lower purchasing power by tens of thousands of dollars. In a market like North Delta, where home prices remain strong due to location, schools, and community appeal, affordability becomes a serious concern for many buyers.

First time buyers are especially affected. Many now look at townhomes or condos instead of detached homes. Some are choosing smaller properties or expanding their search into nearby communities. Others rely more on family support or larger down payments to qualify for financing.

Despite these challenges, serious buyers are still active. They are simply more informed, more patient, and more focused on long-term financial stability.

Impact on Home Listings and Market Activity

Mortgage rates influence not only buyers but also sellers. Many homeowners in North Delta are holding onto their properties because they have low mortgage payments from earlier years. Selling their home would mean purchasing another property at a higher interest rate, which may not make financial sense.

As a result, housing inventory remains limited in many neighbourhoods. This shortage keeps competition steady in well priced homes, especially in family friendly areas close to schools, parks, and transit routes.

However, higher rates have also cooled buyer demand compared to past peak years. This creates a more balanced market, where buyers have more time to make decisions and sellers need to price homes realistically to attract serious interest.

Buyer Behaviour in a Higher Rate Market

Today’s buyers in North Delta are more cautious and prepared than ever before. Many start with mortgage preapprovals before attending open houses. They carefully analyze monthly payments rather than focusing only on purchase prices.

Some buyers are choosing variable-rate mortgages in hopes that rates will decrease over time. Others prefer fixed rates for stability, even if the initial cost is higher. Financial planning and long-term affordability have become top priorities.

Buyers are also more willing to negotiate. They look closely at property conditions, future maintenance costs, and renovation needs. Homes that are moving in ready and priced fairly tend to attract faster offers, while properties needing major updates often sit longer on the market.

Long Term Effects on the North Delta Market

Mortgage rates are shaping long-term trends in North Delta real estate. Instead of rapid price growth, the market is moving toward stability and sustainable development. This shift benefits serious buyers and sellers who value long term planning over short term gains.

As borrowing costs stabilize, more homeowners may consider listing their properties, which could gradually increase inventory. At the same time, steady population growth in Metro Vancouver and the Fraser Valley continues to support housing demand in North Delta.

Over time, this balance may lead to healthier market conditions where prices grow at a moderate pace, affordability improves slightly, and both buyers and sellers feel more confident about their decisions.

Impact on Investors and Rental Housing

Mortgage rates also influence real estate investors. Higher borrowing costs reduce short-term profits, especially in rental properties. However, many investors still see long term value in North Delta due to strong rental demand, proximity to major employment centers, and ongoing population growth.

Some investors are shifting toward multi-family properties or long-term rental strategies instead of quick resale projects. Others are waiting for clearer signals on interest rates before expanding their portfolios.

For renters, this investor caution can mean fewer rental listings in the short term, which keeps rental demand strong. This dynamic continues to shape the broader housing landscape in the community.

What Buyers and Sellers Should Do in 2026

In today’s mortgage environment, preparation is key. Buyers should work closely with mortgage professionals to understand loan options, stress test requirements, and long term affordability. Having a strong pre approval and clear budget can make a big difference in competitive situations.

Sellers should focus on pricing accurately based on current market conditions. Overpricing can lead to longer listing times and reduced buyer interest. Well staged homes with realistic pricing continue to perform well in North Delta.

Both buyers and sellers benefit from working with experienced local real estate professionals who understand neighbourhood trends, buyer expectations, and financing challenges unique to the North Delta market.

Conclusion

Mortgage rates in 2026 are reshaping the North Delta real estate market in meaningful ways. Higher borrowing costs affect affordability, buyer confidence, seller behaviour, and overall market activity. While the market is no longer as fast-paced as in past years, it is more stable, predictable, and focused on long-term value.

For buyers, this environment rewards careful planning and financial discipline. For sellers, it emphasizes realistic pricing and strong presentation. As mortgage rates stabilize and housing demand remains steady, North Delta continues to be a desirable place to live, invest, and build long-term wealth.

Understanding how mortgage rates impact the market allows homeowners and buyers to make smarter decisions and move forward with confidence in 2026 and beyond.